Mastering the Sharpe Ratio Equation

📋 In this guide

The Sharpe ratio equation is a fundamental concept in finance used to measure the risk-adjusted return of an investment. Students often encounter difficulties with this equation due to its reliance on both statistical and financial principles, which can be intimidating to those unfamiliar with these fields. In this comprehensive guide, we will unravel the complexities of the Sharpe ratio equation, providing you with the tools to understand and apply it effectively. By the end of this article, not only will you comprehend the essentials of the Sharpe ratio equation, but you'll also be able to calculate it confidently and apply it to real-world situations.

The Sharpe ratio equation is crucial for investors as it offers a standardized way to assess the performance of various investments while taking into account the associated risks. This equation is particularly useful when comparing different investment opportunities, as it highlights how much excess return an investment provides per unit of risk. Students may struggle with the Sharpe ratio equation because it requires an understanding of statistical concepts like standard deviation, as well as financial metrics such as expected returns and risk-free rates.

Through this guide, you'll learn the step-by-step process of calculating the Sharpe ratio equation, explore worked examples, and discover common mistakes to avoid. Additionally, we'll delve into the real-world applications of the Sharpe ratio, illustrating its importance in investment decisions. Whether you're tackling algebra equations or exploring more advanced topics like the quadratic equation or kinematic equations, mastering the Sharpe ratio equation will enhance your analytical toolkit.

Step-by-Step: How to Solve Sharpe Ratio Equation

Step 1: Understand the Components

To effectively use the Sharpe ratio equation, it's crucial to understand its components. The expected return is the anticipated return on an investment over a specified period. The risk-free rate represents the return on an investment with no risk, typically government bonds. Lastly, the standard deviation measures the dispersion of returns around the expected return, indicating the investment's volatility. Grasping these components is vital for applying the Sharpe ratio equation accurately.

Step 2: Gather the Necessary Data

Before calculating the Sharpe ratio, gather all the required data, including the expected return, the risk-free rate, and the standard deviation of the investment's returns. This information can often be found in financial reports or investment analysis tools. Having precise data ensures that your Sharpe ratio calculation will be accurate, allowing for meaningful comparisons between different investments.

Step 3: Plug Values into the Equation

Once you have all the necessary data, it's time to substitute these values into the Sharpe ratio equation: (Expected Return - Risk-Free Rate) / Standard Deviation of Returns. Carefully perform each arithmetic operation, ensuring that you adhere to the order of operations (parentheses, multiplication/division, addition/subtraction). This step is crucial for obtaining an accurate Sharpe ratio.

Step 4: Interpret the Result

After calculating the Sharpe ratio, interpret the result to make informed investment decisions. A higher Sharpe ratio indicates a more favorable risk-adjusted return, suggesting that the investment provides a better return per unit of risk. Conversely, a lower Sharpe ratio may signal that the investment is not adequately compensating for the risk taken. Use this insight to compare different investments and optimize your portfolio.

🤖 Stuck on a math problem?

Take a screenshot and let our AI solve it step-by-step in seconds

⚡ Try MathSolver Free →Worked Examples

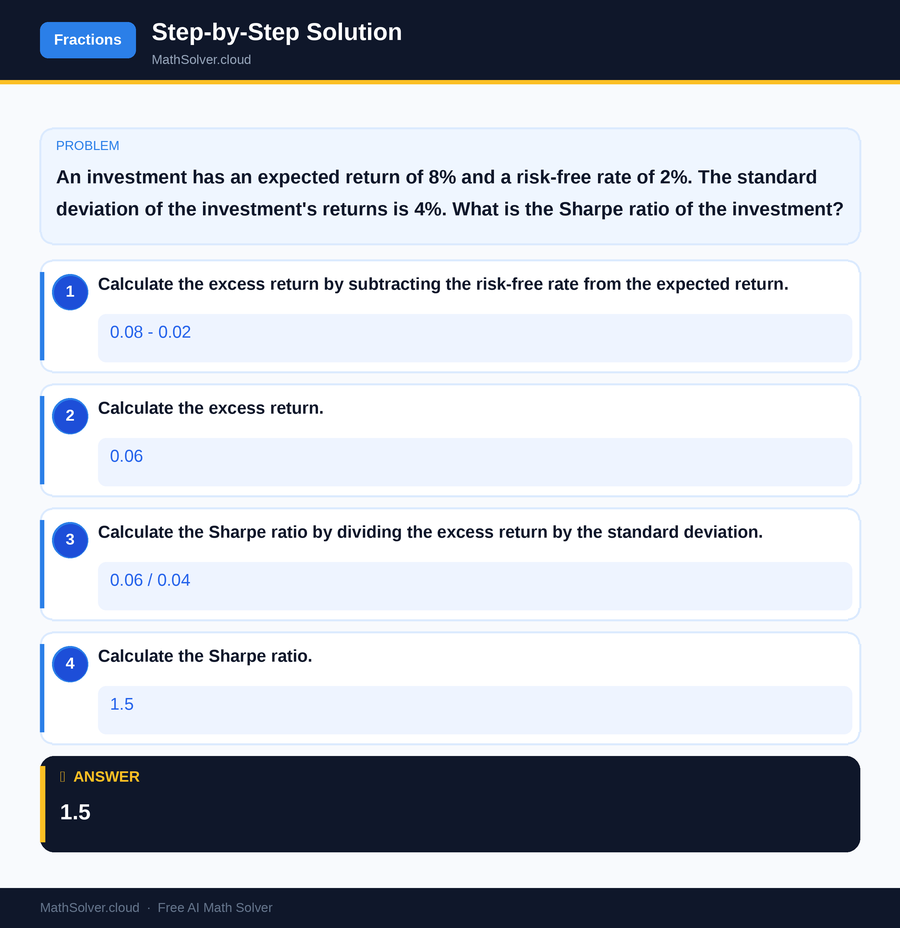

Example 1

MathSolver Chrome extension solving this problem step-by-step

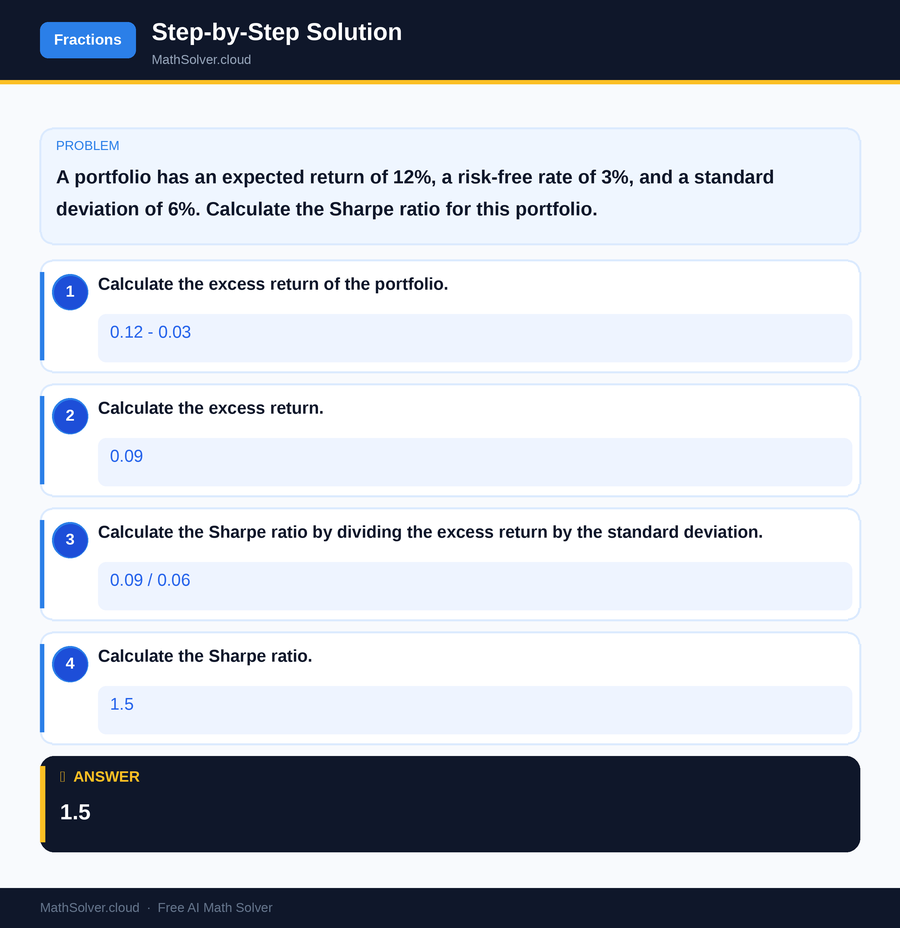

Example 2

MathSolver Chrome extension solving this problem step-by-step

Common Mistakes to Avoid

One common mistake when using the Sharpe ratio equation is miscalculating the expected return or risk-free rate, leading to inaccurate results. Always double-check your data sources and ensure that you are using the correct figures. Another error is neglecting to express all figures in consistent units, such as percentages or decimals, which can skew your calculations.

Additionally, students often overlook the impact of selecting an inappropriate risk-free rate. Choosing a risk-free rate that doesn't align with the investment's time horizon can distort the Sharpe ratio. To avoid this, select a risk-free rate that matches the duration of your investment analysis. By being meticulous with your data and calculations, you can avoid these common pitfalls.

Real-World Applications

The Sharpe ratio equation is widely used in finance to evaluate the performance of mutual funds, ETFs, and other investment portfolios. Financial analysts and portfolio managers rely on the Sharpe ratio to compare the risk-adjusted returns of different investment options, guiding their decisions in constructing diversified portfolios.

Beyond institutional use, individual investors also employ the Sharpe ratio to assess personal investment strategies. By understanding the risk-adjusted returns of their portfolios, investors can make informed decisions about reallocating assets or adjusting their risk exposure. The Sharpe ratio's versatility and clarity make it a vital tool in the realm of investment analysis.

Frequently Asked Questions

❓ What is the purpose of the Sharpe ratio equation?

❓ How is the Sharpe ratio different from other financial ratios?

❓ How can AI help with the Sharpe ratio equation?

❓ Can the Sharpe ratio be negative?

❓ What is a good Sharpe ratio?

🚀 Solve any math problem instantly

2,000+ students use MathSolver every day — join them for free

📥 Add to Chrome — It's Free